Summary

- The stock market performed well in the first quarter of 2024, with the S&P 500 Index increasing over 10%. This was due to factors such as better-than-expected earnings and rising valuations.

- Economic data showed some positive signs, such as a growing job market and an uptick in U.S. manufacturing; however, inflation readings have come in higher than expected for multiple months in a row. In response, bond yields increased during the month of April, which led to a decline in bond prices as higher yields make existing bonds less attractive.

- Bonds weren’t the only asset class to take a beating during the month. Stocks in the U.S. and abroad also fared poorly, as higher real yields on bonds and fewer expected interest rate cuts caused valuations and prices to fall.

On April 3rd a 7.2 magnitude earthquake struck Taiwan, which was the most intense tremor for the country since 1999. The aftermath was devastating. Buildings collapsed, and over 900 people were injured, along with 9 tragic casualties.1

Not long after—in fact, only two days later—a 4.8-magnitude earthquake occurred near New York City. Thankfully, no major damage, injuries, or deaths were reported.2

These natural disasters mirrored the shaky start experienced by global stock and bond markets throughout the month of April, as investors once again faced uncertainty surrounding inflation and interest rates. Before we dive deeper into the specifics, a recap of the first quarter will provide an important backdrop into understanding the underlying movement of financial assets for the month of April.

Q1 Recap

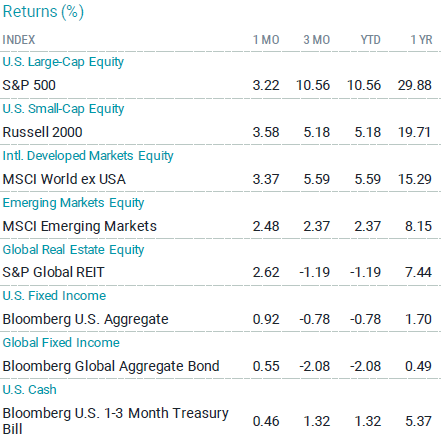

Coming off the back of a rip-roaring rally at the end of 2023, the train kept on rolling during the first quarter of 2024. The S&P 500 Index rose (+10.6%) in Q1 and (+29.9%) in the last 12 months. Strong performance can be explained by a convergence of factors, including better-than-expected earnings and rising valuations. It’s noteworthy that a broadening out amongst size and styles took place. Over 85% of stocks within the S&P 500 Index traded above their 50-day moving average.

Non-U.S. developed stocks (MSCI World ex USA Index) inched out a slight outperformance versus U.S. stocks in March, but their year-to-date gains were more modest. Emerging market stocks, as represented by the MSCI Emerging Markets Index, also rose during March and the quarter, but they underperformed their developed market counterparts.

Source: Avantis Investors. Data as of 3/31/2024. See important disclosures at the end of this material.

The Federal Reserve held rates in place at their March meeting, but continued to forecast three cuts in 2024. A reset of expectations for interest rates occurred from market participants, from six cuts down to three, and the result was increasing Treasury yields. With increasing Treasury yields came declining fixed income performance. The Bloomberg U.S. Aggregate Bond Index returned (+0.92%) in March, but this return was not enough to offset earlier declines, and the index returned (-0.78%) for the quarter.

In the real economy, interest rate-sensitive sectors—though constituting a smaller portion of the economic pie—are still encountering challenges, while the services sector remains on its growth trajectory. Falling inflation and increasing real wages for workers has helped to offset decreasing excess savings and tougher lending conditions. Moreover, the labor market is expanding at brisk pace due to increasing participation, with 265,000 jobs added on average over the last three months ending in February.

Overall, March and the first quarter of 2024 showed respectable returns and economic data.

April Showers

Like a roller coaster, commendable returns and promising economic data can suddenly take a sharp turn, leaving investors feeling exhilarated one moment and queasy the next.

The first abrupt turn was a stronger-than-expected U.S. manufacturing report in early April, rising into expansionary territory. Bond yields rose initially due to increasing growth prospects, and then continued higher when consumer prices for the month of March exceeded estimates.

In January and February, headline inflation rose by 3.1% and 3.2%, respectively, compared to the previous year. Initially, the market didn't pay much attention to these increases, attributing them to the usual seasonal patterns in the data. However, as we've seen three consecutive months of significant increases, worry has started to set in. This concern is valid, particularly because it suggests a growing likelihood of inflation becoming more deeply entrenched, especially in sectors like housing and transportation.

As a consequence of higher-than-expected inflation, bond yields rose, driving bond prices down, real-yields increased, interest rate cut expectations soured, and stocks lost a bit of their footing.

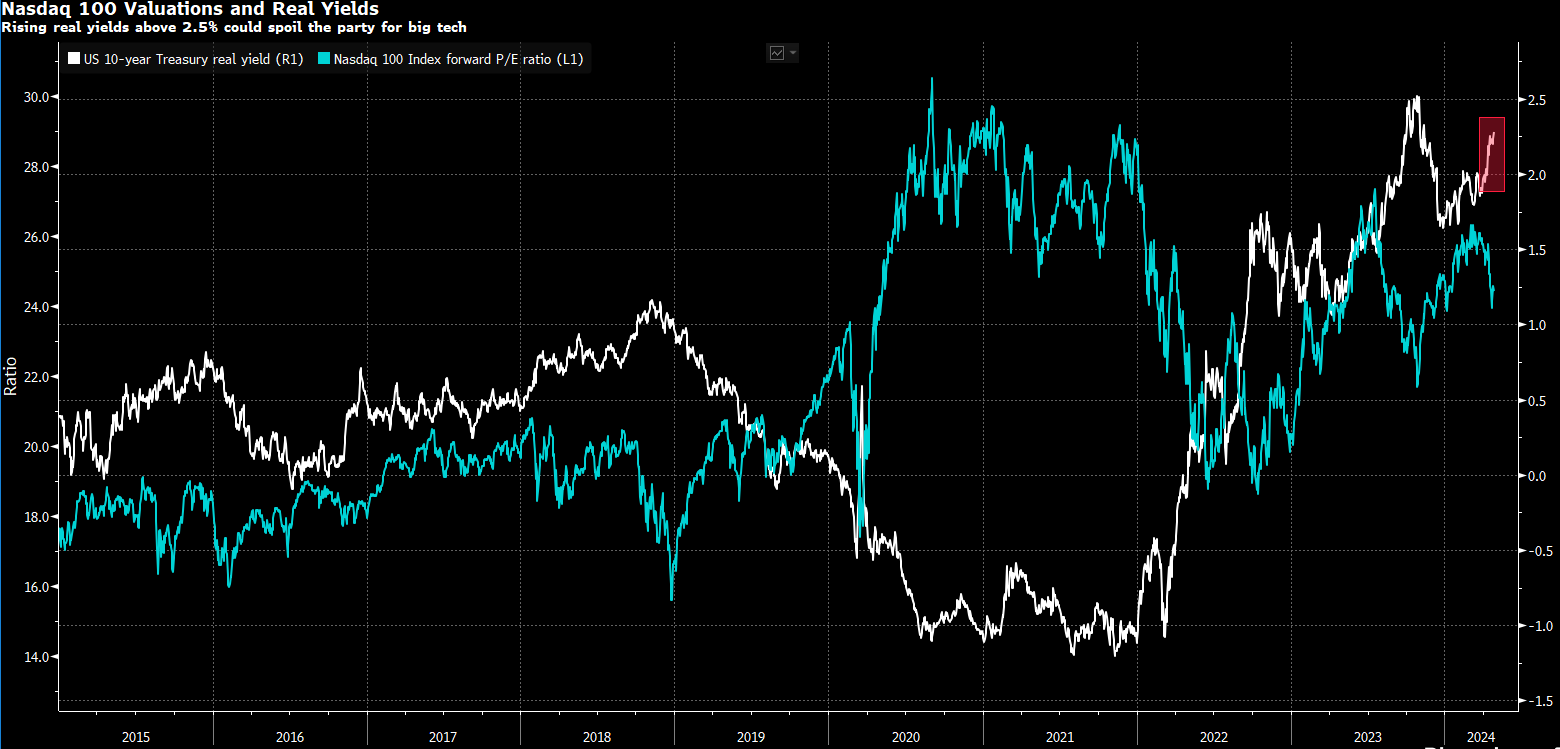

Real yields (white line) in the chart below illustrate the yield on a 10-year Treasury bond after adjusting for inflation. In other words, it is the return an investor earns on an investment after accounting for the effects of inflation.

Source: Bloomberg. Data from 1/1/2015 to 4/25/2024.

Higher real yields on bonds can act as competition for equities should they get high enough. In this case, the rise in real yields drove valuations and prices down for large cap growth stocks. The maximum drawdown experienced in April for the NASDAQ 100 Index was a little more than (-7%). Not a fun ride.

For April's showers to bring May's market flowers, inflation must retreat, corporate earnings must surpass expectations, and bond yields must stabilize or recede.

IMPORTANT DISCLAIMERS AND DISCLOSURES

1. Reuters. (2024, April 3). Strong 7.2 magnitude earthquake hits Taipei. Retrieved from https://www.reuters.com/world/asia-pacific/strong-72-magnitude-earthquake-hits-taipei-2024-04-03/

2. Reuters. (2024, April 5). Magnitude 5.5 earthquake strikes New York, New Jersey: EMSC. Retrieved from https://www.reuters.com/world/us/magnitude-55-earthquake-strikes-new-york-new-jersey-emsc-2024-04-05/#:~:text=NEW%20YORK%2C%20April%205%20(Reuters,rarely%20experiences%20notable%20seismic%20activity.

3. Bureau of Labor Statistics.

The S&P Global REIT Index measures the performance of publicly traded equity REITs listed in both developed and emerging markets. It is a member of the S&P Global Property Index Series.

The Bloomberg US Aggregate Bond TR Index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM passthroughs), ABS, and CMBS.

The S&P 500 Index is widely regarded as the best single gauge of the U.S. equities market. The index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. The S&P 500 Index focuses on the large-cap segment of the market; however, since it includes a significant portion of the total value of the market, it also represents the market.

The Russell 2000 Index measures the performance of the small-cap segment of the US equity universe. It is a subset of the Russell 3000 and includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

The MSCI World ex USA Index measures the performance of the large and mid cap segments of world, excluding US equity securities. It is free float-adjusted market-capitalization weighted.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

The Bloomberg U.S. 1 – 3 Month Treasury Bill Index tracks the market for treasury bills with 1 to 2.0000 months to maturity issued by the US government.

The Bloomberg Global Aggregate Bond Index is a flagship measure of global investment grade debt from a multitude local currency markets. This multi-currency benchmark includes treasury, government-related, corporate, and securitized fixed-rate bonds from both developed and emerging market issuers.

The NASDAQ 100 Index is a modified capitalization-weighted index of the 100 largest and most active non-financial domestic and international issues listed on the NASDAQ.

This presentation is for educational and illustrative purposes only. It is not intended to offer or deliver investment advice in any way. Past performance is not indicative of future results. The information contained in this presentation has been gathered from sources we believe to be reliable, but we do not guarantee the accuracy or completeness of such information, and we assume no liability for damages resulting from or arising out of the use of such information. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Any index presented does not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index.

Nova R Wealth, Inc. is a registered investment advisor with the U.S. Securities and Exchange Commission. SEC registration does not constitute an endorsement of the firm by the Commission, nor does it indicate that the adviser or investment adviser representative has attained a particular level of skill or ability. Nova R provides investment advisory and related services for clients nationally. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Nova R Wealth, who reserves the right at any time and without notice to change, amend, or cease publication of the information contained herein.