Summary

- Geopolitics vs. Earnings: Even with increasing headlines about the Middle East conflict and rising oil prices, investors refused to panic in April. Instead of selling off, the market stayed focused on the massive wave of AI spending and strong corporate profits, proving that real economic growth is easily overpowering the fear of geopolitical risks.

- Inflation Stalls the Fed: Driven by screaming energy prices, April inflation reports showed headline CPI accelerating to 3.8% and Core PCE stuck above 3%. Rate cuts this year are starting to look less likely.

- Yields Grind Higher: Bond markets reflected this prolonged economic uncertainty as Treasury yields steadily marched upward throughout the month, with the 10-year Treasury ending April near 4.37% before aggressively clearing the 4.60% threshold into May. As a result of rising yields, US broad investment-grade fixed income has entered negative territory.

- An AI-Driven, Bifurcated Rally: Even as the S&P 500 rallied over 13% from its late-March low, the rebound was intensely concentrated—led by a massive 40% surge in semiconductors and a quiet outperformance in AI-linked emerging markets, while the US equal-weight index lagged behind and exposed a widening gap across the rest of the market.

April Recap

You would think a month dominated by war headlines, rising oil prices, stubborn inflation, and higher Treasury yields would have been a straightforward risk-off environment. It wasn’t. Every time crude oil pushed higher, or another headline crossed about the Strait of Hormuz, markets initially reacted the way you would expect them to react, only with a bit less punch than we saw a month ago.

Instead, investors kept circling back to the same conclusion, which is that as long as earnings remain strong and the AI investment cycle keeps accelerating, it is very difficult to become outright bearish on equities, even with geopolitical risk hanging over all our heads.

April was defined by a macro environment that feels increasingly fragile and a market that just wants to push higher anyway.

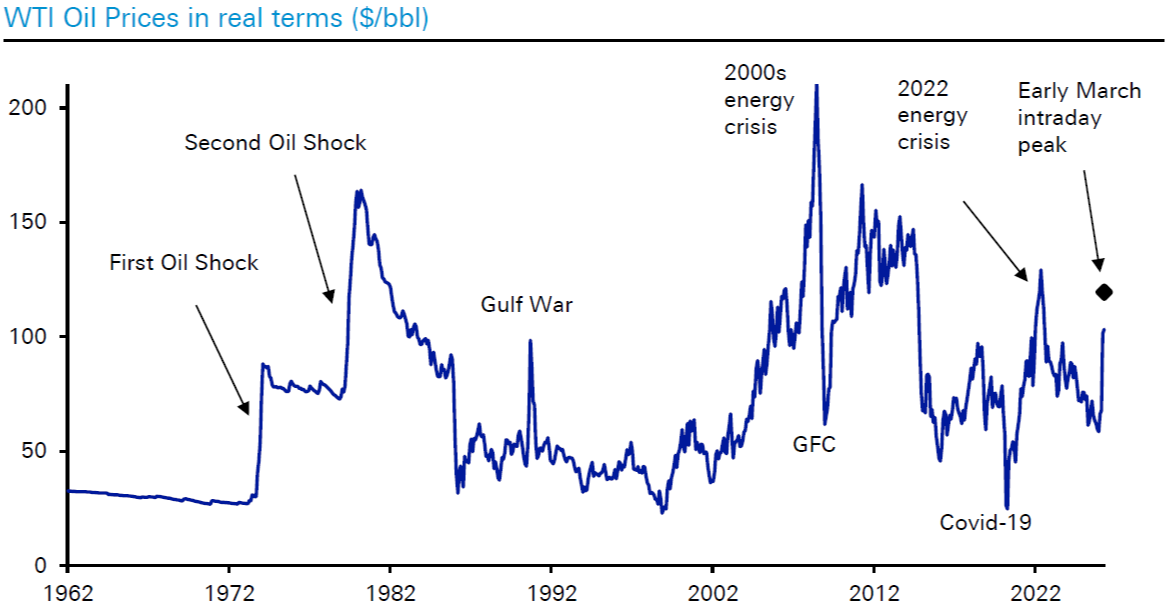

Part of what made the month unusual is that the oil shock, while significant, still has not produced the kind of economic panic investors normally associate with Middle East escalation. Deutsche Bank noted that the current move in oil prices is now becoming one of the larger energy shocks of recent decades, though still well short of the most severe historical episodes. Instead of fearing a systemic crisis, markets and investors seem to view the situation as a stubborn inflation problem that will likely linger without causing long-term devastation.

Source: Deutsche Bank.

Inflation & Fixed Income

With oil prices screaming higher these past few months, we all saw inflation inevitably moving higher. The April inflation reports reinforced the idea that price pressures are no longer cleanly moving back toward the Fed’s target.

Headline CPI accelerated to 3.8% year-over-year in April, up from March’s reading of 3.3%, while Core PCE—the Federal Reserve’s preferred inflation metric—remained stuck above 3%. While these numbers aren't catastrophic, they are high enough to keep policymakers uncomfortable.

As a result of the elevated inflation headlines, the April Federal Open Market Committee (FOMC) meeting revealed a committee that is becoming increasingly divided on what comes next. The important shift here is not necessarily that the Fed is preparing to hike rates again. It is that officials seem far less confident they will be cutting anytime soon if inflation remains trapped near current levels.

Source: Bloomberg. Data from 5/15/2025 to 5/15/2026.

Bond markets reflected that uncertainty throughout the month. Treasury yields grinded higher, with the 10-year Treasury ending April near 4.37%, up slightly from the end of March. As we write this, yields are now pushing over 4.60%. Consequently, broad investment-grade fixed income returns have turned negative for the year.

Corporate Earnings

At the same time, the economy continues to defy cynics.

Labor market data stayed remarkably firm throughout the month. Payroll growth continued beating expectations, and jobless claims remained historically low.

The real story, however, is corporate earnings. Not just earnings beating expectations, but earnings estimates continuing to move higher during a period when many investors expected analysts to start cutting forecasts instead. Goldman Sachs estimated that Q1 year-over-year S&P 500 earnings growth is now tracking near 16% excluding one-time distortions, with one of the lowest rates of earnings misses seen in decades.1

And increasingly, almost every road in this market seems to lead back to AI.

Speaking of AI, it appears AI-related investment could drive roughly 40% of S&P 500 earnings growth this year, with hyperscaler spending plans continuing to climb toward levels equal to roughly 2.5% of US GDP, which is an astounding number when you stop and think about it.1,2 The market is no longer treating AI as a speculative future story. It is playing out before our eyes.

Equity Markets

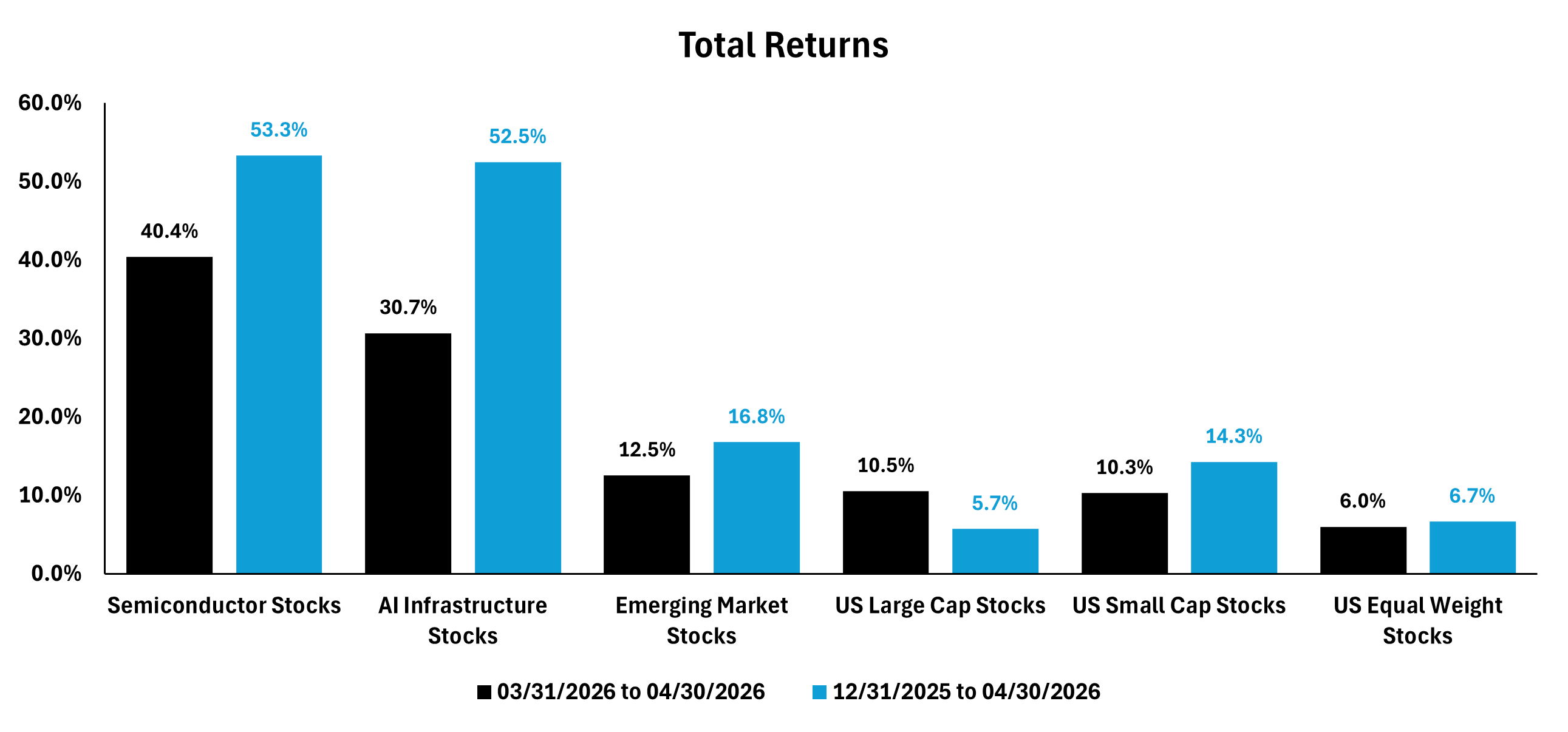

After hitting a market low in late March, the S&P 500 rallied more than 13% by the end of April, pushing the index back into positive territory for the year. Nevertheless, the defining story of this rebound lies with its leaders: semiconductor and AI infrastructure stocks have driven a disproportionate share of the gains since the onset of the Iran conflict.

The SOX Semiconductor Index surged roughly 40% from the market low and AI infrastructure stocks increased about 30%. Meanwhile, the equal-weight S&P 500 Index materially lagged, signaling a slowdown in many other sectors.

Source: Bloomberg; Nova R Wealth. Semiconductor Stocks represented by SOXX ETF, AI Infrastructure Stocks represented by TCAI ETF, Emerging Market Stocks represented by IEMG ETF, US Large Cap Stocks represented by IVV ETF, US Small Cap Stocks represented by IJR ETF, and US Equal Weight Stocks represented by RSP ETF. Past performance is no guarantee of future results.

Outside the United States, emerging markets quietly continued outperforming many developed-market peers. Emerging markets lead most major equity benchmarks year-to-date, as most of the strength is coming from Taiwan, South Korea, and other AI-linked Asian markets. In many ways, those markets now sit directly at the intersection of semiconductor demand, AI infrastructure spending, and improving global earnings trends.

Moving Forward

Taken together, April’s market action delivered a fairly clear message. Investors are not dismissing geopolitical risk, but they are increasingly willing to look through it as long as corporate earnings remain durable, labor markets stay resilient, and AI spending continues generating measurable economic benefits.

Whether markets can maintain that balance will depend on several unresolved questions. If oil prices stay elevated for too long, inflation pressures could become more deeply embedded. Higher Treasury yields could eventually pressure valuations. And the more concentrated market leadership becomes, the more dependent overall index performance becomes on a relatively small group of companies continuing to exceed already-high expectations.

For now, though, markets continue behaving as though earnings matter more than fear.

(1) Snider, B., Hammond, R., Ma, J., Chavez, D., Jayachandran, K., & Sung, C. (2026, May 1). US Weekly Kickstart: Q1 2026 mid-season S&P 500 earnings update. Goldman Sachs Global Investment Research.

(2) Pearkes, G., & Gordon, J. (2026, May 1). Global macro update: The Bespoke Report. Bespoke Investment Group.

IMPORTANT DISCLAIMERS AND DISCLOSURES

This presentation is for educational and illustrative purposes only. It is not intended to offer or deliver investment advice in any way. Past performance is not indicative of future results. The information contained in this presentation has been gathered from sources we believe to be reliable, but we do not guarantee the accuracy or completeness of such information, and we assume no liability for damages resulting from or arising out of the use of such information. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The performance numbers displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Any index presented does not incur management fees, transaction costs or other expenses associated with investable products. It is not possible to directly invest in an index.

Nova R Wealth, Inc. is a registered investment advisor with the U.S. Securities and Exchange Commission. SEC registration does not constitute an endorsement of the firm by the Commission, nor does it indicate that the adviser or investment adviser representative has attained a particular level of skill or ability. Nova R provides investment advisory and related services for clients nationally. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Nova R Wealth, who reserves the right at any time and without notice to change, amend, or cease publication of the information contained herein.